How Revenue-Based Financing Works?

Revenue-based financing refers to securing borrowing (credit) by utilising projected profits. The investor or lender gets a certain percentage of the borrower’s income, commonly known as the revenue share. The lender then receives payment for the principal amount plus the revenue share.

To understand how revenue-based financing works, let us take an example. Let’s say, firm A makes an average of Rs 30 lakh every month. As a result, they expect to make Rs. 3.6 crore a year. It offers this estimate to an RBF supplier and suggests that they pay for it with Rs 30 lakh.

This lender lends the money following an evaluation for a 12% revenue share. As a result, firm A must pay back Rs. 336,000, or Rs. 300 000 + Rs. 360 000. (finance cost or revenue share).

Revenue-based financing considers several parameters like revenues, cash flow, scalability, growth capital, etc., when it comes to auditing. They will lend the agreed amount to the borrower’s account if convinced.

2. Capchase

Capchase was founded in 2020 in New York City, USA. This is also a revenue-based financing company that offers to fund to startups in the B2B SaaS sector and subscription-based revenue-generating sector.

The firm focuses only on US-based companies and offers up to 60% of annual recurring revenue in funding to the applicants. However, it is necessary that for attracting successful investments, the applicant companies must have at least $1M in annual recurring revenue. The applicant companies also need to provide 8 months of revenue history.

Capchase does not ask for any equity share or any personal guarantee, and it charges a flat rate of interest for repayment.

The Different Types of Revenue-Based Financing

RBF can be structured in a few ways. The most common type of structure you’ll come across is one that is similar to the structure of a term loan. You receive a set sum of capital and repay that capital, with interest, over time. However, you may also come across RBF with a structure similar to that of a business line of credit. The full amount of capital is not given up front, but drawn upon over a number of years, so that no interest is accrued until the money is needed.

You may also have RBF that involves making payments to investors in different ways. This is dependent on the terms of the agreement with the investor, but you might make payments until:

- The investor receives a pre-determined payment of the initial loan amount.

- The investor reaches a pre-determined internal rate of return.

- A pre-determined, final date is reached.

Revenue-based financing may differ in structure, but they’re all based on regular payments based on your company’s sales, and the time it takes for you to repay the investment will vary too. However, typically, repayment of the initial investment will range from three to five years.

What is Revenue-Based Financing?

Revenue-based financing refers to the practice of raising capital from an investment source, which in turn receives a portion of the company’s gross revenues in exchange for their investment.

Sometimes referred to as royalty-based financing, revenue-based lending enables investors to continue receiving a percentage until a preset total has been accrued. Typically, the predetermined amount is anywhere from three to five times the original investment.

Revenue-based financing is often considered a hybrid of equity and debt financing, which makes it particularly popular with startups, technology companies, and SaaS (software as a service) businesses.

Originating in the early ’90s, revenue-based lending was pioneered by venture capitalist Arthur Fox, an engineer-turned-investor. In 1992, he began the first small revenue-based fund in ’92, which was quickly followed by a larger fund in ’95.

Both funds returned an internal rate of return (IRR) of more than 50 percent with average recoupment of 28 to 30 months, quickly launching the model of alternative financing into worldwide fame.

Revenue-based loans were initially seen as a promising way to provide entrepreneurs in developing countries with rapid growth capital. In the wake of economic uncertainty, it offered a proven method to catalyze economic development in struggling industries and new enterprises alike.

But revenue-based funding has since expanded globally and gathered momentum due to its success in nations and companies of all kinds.

In 2000, there were just two publicly announced revenue-based funding deals. Less than a decade later, there were 27. Now, the lending option has become so popular and specialized that a single firm completed 500 deals by itself in 2018.

As revenue-based lending has grown in popularity, startups have increasingly turned away from venture capital, and for good reason. In contrast with revenue-based financing, venture capitalists often offer investments on the expectation of extreme, rapid, and often unhealthy early-stage growth.

In fact, it is not uncommon for venture capitalists to create an environment where growth occurs before demand can catch up. According to the comprehensive Startup Genome Report, premature scaling was the primary reason for failure across 3,200 startups. And 74 percent of startups that failed due to premature growth received two to three times more capital than was necessary.

The venture capital funding model puts companies on a fast track to grow through a surplus of available capital. Borrowers are led to believe that, if they just grow more quickly than the competition, they will succeed. And this excessive growth is accompanied by a miasmic spiral of larger and larger funding rounds.

Companies that don’t want to sell or go public after growth are not well-served by this model. Thankfully, revenue-based lending provides an attractive alternative to the “grow or die” mantra typical of venture capital firms.

How Much Do Revenue-Based Financing Companies Cost?

Revenue-based financing companies can vary widely in cost, depending on their individual terms. Generally speaking, they will charge a fee based on a percentage of the company’s annual revenue, with this percentage typically ranging from 1-7%. The duration of the loan and repayment schedule will also have an impact on the total cost. For example, a shorter loan term may have higher upfront fees but lower total costs, while longer-term loans may be more expensive overall but offer better cash flow flexibility. Additionally, some revenue-based financing companies might charge additional service fees for the convenience of setting up and managing the agreement. Ultimately, it is important to carefully consider all factors involved before making a decision about working with one of these companies.

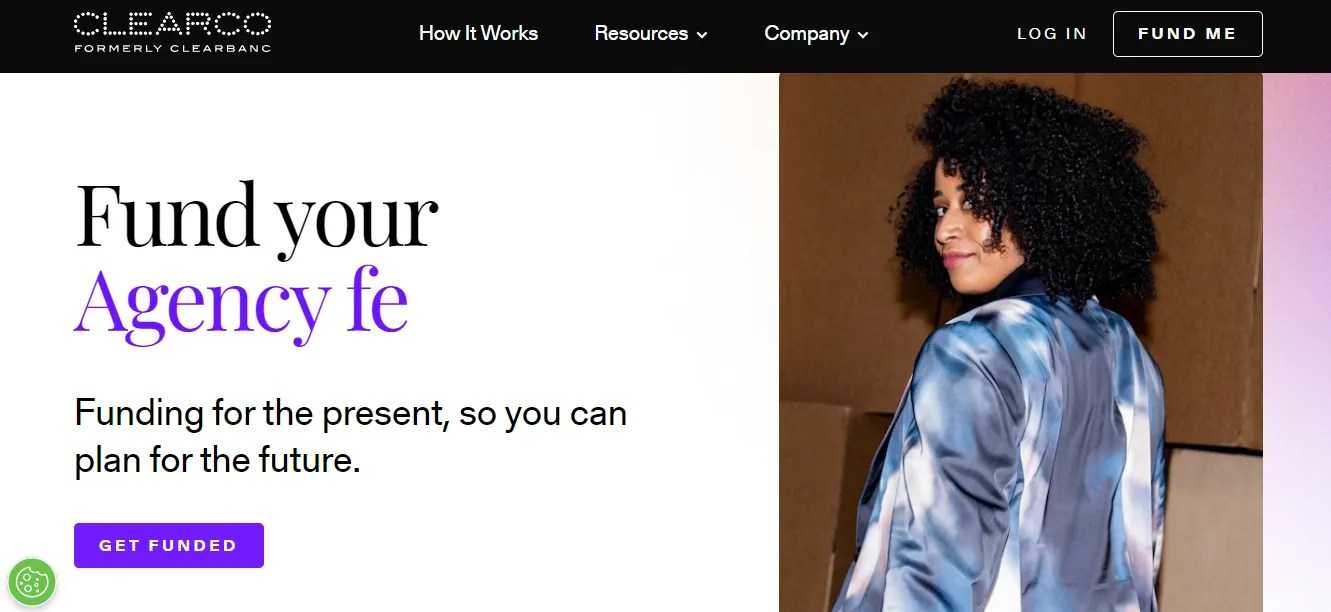

3. Clearco

Clearco was previously known as ClearBanc. It is a revenue-based financing firm that was founded in 2015. As of now, Clearco has a physical presence in Canada, the USA, the UK, Australia, and Ireland.

This revenue-based financing firm offers to fund businesses in the eCommerce, mobile apps, and SaaS sectors. The firm offers to fund anywhere between $10k and $20M. However, applicant companies must have a revenue of more than $10k per month, and the company should be a corporation or an LLC.

Clearco doesn’t restrict its investment to companies operating in the countries where Clearco has a physical presence. In fact, this firm invests globally.

8. Re:cap

Re:cap is a Germany-based revenue-based financing firm that offers to fund companies operating in Europe. This firm does not offer to fund companies in any other country. Founded in 2021, Re:cap offers to fund only software companies with subscription-based business models.

This firm offers up to 50% of annual recurring revenue. Unfortunately, the firm does not disclose the eligibility conditions anywhere on its website.

Re:cap charges a flat interest rate for repayment and does not ask for equity share collateral in return for the investments like traditional venture capital firms or bank loans, respectively.

Benefits for Lenders

While the benefits for borrowers are readily apparent, what’s in it for lenders? Perhaps most compellingly, revenue-based loans generate high returns when they are structured in the right way for the right companies.

For instance, one lender may decide to structure a revenue-based financing deal as debt and utilize an equity multiple of 2.5. If the borrower receives $2 million as the principal investment, they would pay off $5 million over time to the lender.

Depending on how quickly the loan is paid off, the fund’s investor would receive an internal rate of return (IRR) ranging from 25 to 40 percent. Of course, if sales drop, the IRR could fall closer to 5 percent.

The diligent investor rarely invests in a company that fails before expected repayment and may benefit handsomely from a borrower that repays quickly. Unlike traditional loans, revenue-based financing is incredibly durable in the wake of an economic crisis.

Consider the impact of COVID-19, for example. While some borrowers are struggling, they are still paying based on their lowered revenues, leading investors to expect a return of 20 percent on average.

Whether the economy is healthy or stoppered, lenders still expect to receive the same multiple on the principal loan amount. The difference simply lies in how quickly they start making a return on the initial investment.

Aside from metrics of profitability, the lender and borrower both benefit from sharing the same goals. Both want the company to be successful and for repayment to be quicker — the mutually advantageous loan structure prevents either party from getting burned.

Lenders will invest in a company dependent on a few key factors. Profit, gross margins, historic revenue, and projected earnings all serve in the final decision, as does the company’s business model and management structure.

11. Uncapped

Founded in 2019, Uncapped is a popular revenue-based financing firm that is located in the United Kingdom. However, the firm offers investments to companies all across Europe.

Just like most of the other revenue-based financing firms listed here, Uncapped also focuses only on eCommerce startups, startups with a recurring revenue or subscription model, SaaS & mobile app development startups, and startups in the direct-to-consumer business segments.

Uncapped offers to invest anywhere between €10k and €5M. The startups applying for funding must show a minimum monthly revenue of €10k for a minimum of 6 months at a stretch. Uncapped never asks for equity shares or collateral.

Revenue Based Financing Cons ❌

- High volume of cash flow. Need to be generating significant revenue on a consistent basis, as you’ll be using this to make repayments.

- A built-in buffer is crucial. Must have healthy gross margins in your business to account for the portion of revenue that will be redirected to paying off any loans.

- Consistent expectation of repayments. Once you have the responsibility to make good on the capital you have been given, returning your investment as a percentage of sales means there is a constant drip of paying back what you owe.

- High APR. When you run the numbers on revenue-based financing, you will often find that the APR is much higher than other financing options such as line of credit.

How does Revenue Based Financing work? 🤔

If provided with capital in this manner, it is assumed that your company will set aside a percentage of revenue in order to repay the advance. This typically occurs on a set frequency, such as on a monthly basis.

Should certain months yield more revenue for your business, this results in a greater monthly payment and a shorter overall repayment period. The inverse is also true. A drop in revenue on certain months means a smaller monthly payment and lengthening of the repayment cycle.

In a practical sense, getting financing involves signing up with a provider and connecting your business’s financial and marketplace accounts to determine eligibility. You then select an offer that is based on projected earnings, and begin repaying your advance according to the revenue your business is bringing in.

Generally it is expected that the capital invested is repaid within a few months to a few years.

Examples of Revenue-Based Financing

For more clarity, it may be helpful to review some hypothetical examples of companies in their journey to secure revenue-based financing deals with investors.

First, consider the example of a medical technology company seeking to increase the size of a funding round without triggering premature equity dilution. A revenue-based loan satisfies that goal, providing flexible repayment and the ability to draw down funding later on.

Perhaps most compellingly, the upfront capital could be used to gain a greater market share and reach new healthcare facilities, without disrupting its ownership structure. This approach allows the company to focus on scaling their operations without worrying about changes in equity.

Alternatively, imagine a SaaS company that provides an integrated marketing platform for other small- and mid-sized companies, and is looking to expand itself. Revenue-based financing provides a runway for that growth, as the business benefits from the fact that repayments are dependent on its MRR, which is highly predictable due to the structure of the business.

Finally, consider a data user identification company that decides to go the revenue-based financing route to meet its goals of expanding into new markets and improving sales.

In an increasingly complicated era where consumers interact across many digital channels, the company shows very promising signs of future growth. The investor would be willing to provide a fairly termed revenue-based loan agreement with a high principal investment amount and additional capital disbursements upon meeting certain milestones.

What is Revenue-Based Finance?

Revenue-based financing (RBF) refers to the strategy to raise capital for a firm. It is generally taken from investors who are compensated with a portion of the company’s ongoing gross revenues in return for their investment.

In an investment using revenue-based financing, investors get a recurring cut of the company’s profits up until a preset sum is paid. This fixed sum is often a multiple of the principal investment and typically varies between three and five times the initial investment.

It is a logical progression for early-stage venture investment and private equity financing. However, as RBI is a new concept, little information is available to the general public.

Questions To Ask When Considering Revenue-Based Financing Companies

- What is the interest rate for this loan?

- Are there any penalties or fees associated with this loan?

- How quickly can I receive the funds?

- What kind of repayment schedule will I have to follow?

- Is there a minimum and maximum amount that can be borrowed?

- Does the lender conduct background checks prior to offering financing?

- Are there any restrictions on who or what can be financed through this option?

- Does the company provide financial advice, such as cash flow projections or budgeting tools, to help manage cash flow and debts?

- Can additional capital be obtained if needed in the future?

- Are there any other benefits available (e.g., discounts on vendor services; early payment discounts)?

6. FlowCapital

FlowCapital is one of the oldest FinTech companies operating in Canada. It serves in US, UK, and Canada and provides non-dilutive growth capital to SaaS and other tech businesses.

Its core products are Venture debt and Revenue-based financing. Venture debt is ideal for those willing to issue stock warrants (Offering investors the right to purchase the stock from the company in the future.) It doesn’t eliminate the dilution but minimizes it greatly.

You can receive up to $7M in VD and pay it back within five years. You can also choose a Non-Amortizing Term Loan and make a balloon payment.

The Revenue-based product offers almost similar benefits, but its payment terms are more flexible. It’s well-suited for SaaS businesses with long-term subscription contracts.

What makes FlowCapital different from other financial service providers is the payment schedule and eligibility criteria. Unlike other lenders, it delivers debt financing to mature startups with annual revenue of at least $4M. Meaning, it’s only a viable option if you need funds to scale your business.

Short Summary

Company’s Headquarters: Toronto, Canada

Product: Venture debt, Revenue-based financing

Businesses it Supports: Mature startups

Funding: Up to $7M

Best for: Expansion, cash runway

Who can Benefit from Revenue Based Finance?

Revenue-based financing is advantageous for many different company models, but some industries stand out to gain the most.

E-commerce Businesses

Online retailers are particularly well-suited to revenue-based financing since it gives them the flexibility to invest in marketing or inventory to fulfil demand swiftly.

Due to their internet sales, these companies make it simple for lenders to predict their success using information from their marketing and accounting accounts.

Companies with Seasonal Performance

Online retailers are particularly well-suited to revenue-based financing since it gives them the flexibility to invest in marketing or inventory to fulfil demand swiftly.

Due to their internet sales, these companies make it simple for lenders to predict their success using information from their marketing and accounting accounts.

SaaS and Subscription Businesses

Businesses with predictable and steady monthly incomes are more likely to benefit from revenue-based financing. This is because revenue-based repayments are based on MRR.

SaaS and subscription firms get payments every month. They know exactly how much income to anticipate each month. They can make their monthly payments better with reduced administrative costs and this consistency.

Uncapped raises £10M to offer ‘revenue-based’ finance to growing businesses

Posted December 2, 2019

In Europe, Fundings & Exits, Startups, TC, TechCrunch — Funding & Exits, Technology News

Uncapped, a London headquartered and Warsaw-based startup that wants to provide “revenue-based” finance to growing European businesses, is officially launching today and disclosing that it has raised £10 million in funding.

The capital is a mixture of equity funding and debt (money it can use for lending), and sees the fintech company backed by Rocket Internet’s Global Founders Capital, White Star Capital, and Seedcamp.

I understand a number of angel investors also participated. They include Robert Dighero (Partner at Passion Capital), Carlos Gonzalez-Cadenas (COO of GoCardless) and David Nolan and Kevin Glynn (founders of Butternut Box).

Founded by “serial entrepreneur” Asher Ismail (who was most recently CEO of Midrive), and former VC Piotr Pisarz, Uncapped has set out to use various marketing, sales and accounting data to be able to offer finance for young businesses based on their current (and projected) revenue.

Specifically, Uncapped says it will enable founders to access working capital between £10,000 and £1 million for a flat fee of 6% interest. It’s being pitched as a smart alternative for growing companies that don’t want to give away equity in return for capital to help grow.

“The first decision that entrepreneurs need to make when raising finance is whether to give away a portion of equity in their company, or take on debt,” explains Ismail. “Equity is a slow and very expensive way to fund growth, while loans add more risk. We’re creating an alternative that sits between debt and equity financing, while offering the benefits of both. We started Uncapped so that entrepreneurs wouldn’t have to give up a piece of their company or put up their house”.

Ismail says that Uncapped provides entrepreneurs with access to capital without the need for “personal guarantees, credit checks, warrants, or equity,” and promises to move a lot quicker than investors, or for that matter, more traditional forms of debt finance, can.

“We don’t require customers to share any business plans, cap tables, or pitch decks,” he adds. “All we need is to verify their business performance. We connect to the business’ existing sales and marketing platforms, like Stripe, Shopify and Facebook. Revenue-based finance also gives founders the flexibility to repay less when their sales slow or the market hits a downturn”.

The only stipulation is that businesses must be based on online payments and have at least nine months trading history. This makes Uncapped particularly suitable for companies operating e-commerce, SaaS, direct-to-consumer, gaming and app development businesses.

“For example, our first customer was online menswear brand, L’Estrange,” Uncapped Pisarz tells me. “For e-commerce businesses, December is typically the most challenging time to invest in growth, as inventory and marketing costs are at a peak but Christmas sales have not yet come through. We were able to provide the business with an advance within three days”.

Meanwhile, Ismail claims that Uncapped is the first company of its kind to launch in Europe (which is somewhat of a stretch) and that venture capital — although very different — is probably the closest alternative form of financing.

“Despite the $35 billion invested in Europe by VCs this year, many companies do not fit the venture model,” he says. “They might be a family business that doesn’t intend to sell, an entrepreneur focused on more of a niche market, or minority who may be overlooked by traditional funders. Whilst VCs will often meet 1,500 companies and back just five of them a year, we have the ability to provide 100s of businesses with growth capital for a flat fee much faster and without sacrificing equity at an early stage”.

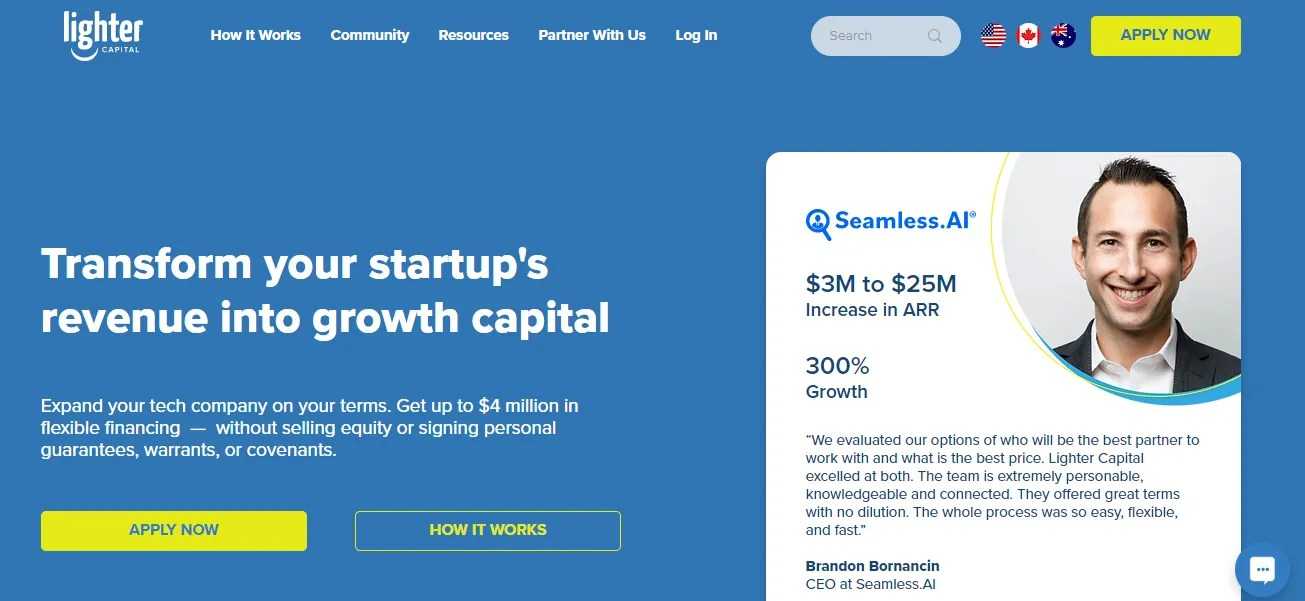

9. Lighter Capital

Lighter Capital supports tech startups in the US, Canada, and Australia. It was founded in 2010, and since then, it has deployed $400k to founders and growing businesses.

If you earn 15k in monthly revenues, you can opt for three of its non-dilutive financing products; Revenue-based, term loans, and contract-based loans. (The contract product delivers upfront cash against 12-month short contracts or a large receivable.)

For repayment, Lighter Capital allows up to three years of relaxation. You can fix monthly installments or tie the repayment schedule to your future sales. It’s up to you.

The website shows transparent pricing with a valuation calculator to let you generate the estimated cost of capital. But generally, you can receive a $1M to $4M loan based on your business health report. In addition to funding, Lighter Capital also gives you access to its community network and offers other perks like software discounts.

Overall, it’s worth exploring.

Short Summary

Company’s Headquarters: Seattle, USA

Product: Revenue-based financing

Businesses it Supports: SaaS companies

Funding: Up to $4M

Best for: Cash runway, Growth Capital

2. Clear Co (Formally ClearBanc)

Clear Co provides lending options to US-based eCommerce businesses. The platform delivers upfront cash to meet various operational needs, such as stock purchases, vendor payments, marketing, and logistics.

You can receive up to $20 million from Clear Co and repay the debt as you earn money along the way. Almost, 7000 customers are currently using its services to grow their startups.

The eligibility criteria of Clear Co are slightly strict but user-friendly. There are around 19 products it doesn’t support. Otherwise, anyone who generates a minimum of $10k per month can apply for the funding. Here’s a list of niches not applicable for the loan.

After the signup process, it takes 2 to 4 business days to receive the funding. You’ll be charged 5.25% to 10.25% fees with no compounding interest structure.

It shares a straightforward payment schedule and sends invoices for each debit transaction. During slow months, the platform automatically reduces the debt and extends the schedule accordingly to adjust the amount.

Short Summary

Company’s Headquarters: Toronto, Canada

Product: Revenue-based financing

Businesses it Supports: eCommerce, service-based, and SaaS companies

Funding: $10 to $20M

Best for: Operational expenditure

5. Liberis

Founded in the United Kingdom in 2007, Liberis is a revenue-based financing firm that offers an alternative to venture funding. This firm focuses on small businesses irrespective of the sector. Interestingly, businesses that have been operational for less than 4 months can also apply for funding from Liberis.

What is interesting is that Liberis does not disclose the exact investment amount. However, it does require the applicants to have a minimum of £2,500 monthly revenue. What is interesting amount Liberis is that this firm is open for investment in companies across the UK, the US, and entire Europe.

Advantages of Revenue-Based Financing

Revenue-based financing has many advantages compared to venture capital firms’ loans. Here is the list of the advantages that you should know:

Non-dilutive

As a company owner, you retain complete control over your enterprise. You are not required to give up any equity financing interests in exchange for the funding you obtain. It is crucial for firms that are expanding quickly and require finance for it.

No Personal Guarantee Needed

Some revenue-based financing lenders might not require a personal guarantee or security during the application process, making it a less risky and quicker choice for borrowing funds.

Loan Repayments are Flexible

Revenue-based financing has payback terms that depend on how well your company performs. When sales are brisk, you pay more; when they’re sluggish, you pay less. This also implies that you will always have adequate growth capital to get through your post-holiday sales downturn.

Fast-Growing Companies Settle Quicker

Companies with rapid growth and an expected high future revenue make quick repayments. As a result, they end up giving low revenue.

Cheaper than Equity

Repayments are often far less expensive than interest, making it a much more cost-effective choice than getting your first investment from angel investors or venture capital organisations.

Fast Funding

Compared to venture capital firms’ funds and bank loans, you get revenue-based financing within a week. On the other hand, the other forms of bank loans take months for the funds to be released.

Works well with other Funding Sources

Early-stage firms benefit from revenue-based financing by gaining momentum, making other investment sources more available and affordable.